4 Utility, Risk and Decisions

“I would never die for my beliefs because I might be wrong.” – Bertrand Russell

Statistical decision theory asks: given what the data tells us, what should we do? The problem typically splits in two. First, learn something from data—estimate parameters, fit a model. Second, use that learning to choose an action. In finance, this means estimating means and covariances from historical data, then constructing a portfolio. In statistics, it means evaluating which estimator or hypothesis test performs best under a given criterion.

The examples in the previous chapter focused on learning about unknown quantities from data, expressed through posterior distributions. In many applications, however, we must turn a posterior into an action: approve a loan, deploy a model, choose a medical treatment, or ship a product variant. This step requires an additional ingredient beyond probability modeling: a loss function that formalizes what we mean by a good or bad decision.

For a parameter \(\theta\) and a decision (or estimate) \(a\), a loss \(\mathcal{L}(\theta, a)\) assigns a numerical penalty to choosing \(a\) when the truth is \(\theta\). Given data \(y\), Bayesian decision making compares actions using posterior expected loss, \[ \E{\mathcal{L}(\theta, a)\mid y}. \] The optimal Bayesian action is the posterior Bayes rule \[ a^*(y) = \arg\min_a \E{\mathcal{L}(\theta, a)\mid y}. \]

Several estimators that are common in statistics can be interpreted as Bayes rules under simple choices of loss. For example, the posterior mean minimizes squared error loss \(\mathcal{L}(\theta,a)=(\theta-a)^2\), while the posterior median minimizes absolute error loss \(\mathcal{L}(\theta,a)=|\theta-a|\). Under 0–1 loss for point classification, the posterior mode becomes optimal. This perspective makes point estimation a special case of a more general principle: choose the action that is optimal under the posterior distribution and the costs of being wrong.

This chapter develops this decision-theoretic framework systematically, connecting loss functions to utility, risk, and optimal actions under uncertainty.

4.1 Expected Utility

Let \(P,Q\) be two possible risky gambles or probability bets. An agent’s preferences can then be specified as an ordering on probability bets where we write \(P\) is preferred to \(Q\) as \(P \succeq Q\) and indifference as \(P \sim Q\). A compound or mixture bet is defined by the probability assignment \(p P + (1 - p ) Q\) for a prospect weight \(0 \leq p \leq 1\).

Ramsey-de Finetti-Savage show that if an agent’s preferences satisfy a number of plausible axioms – completeness, transitivity, continuity and independence – then they can be represented by the expectation of a utility function. The theory is a normative one and not necessarily descriptive. It suggests how a rational agent should formulate beliefs and preferences and not how they actually behave.

This representation of preferences in terms of expected utility \(U(P)\) of a risky gamble is then equivalent to \[ P \succeq Q \; \; \iff \; \; U (P) \geq U (Q ) \] Therefore, the higher the value taken by the utility function the more the gamble is preferred. Specifically, the axioms lead to existence of expected utility and uniqueness of probability.

The two key facts then are uniqueness of probability and existence of expected utility. Formally,

- If \(P \succeq R \succeq Q\) and \(w P + (1 - w ) Q \sim R\) then \(w\) is unique.

- There exists an expected utility \(U(\cdot )\) such that \(P \succeq Q ~ \iff ~ U (P) \geq U (Q)\). Furthermore \[ U \left (w P + (1 - w ) Q \right ) = wU (P) +(1 - w ) U(Q) \] for any \(P, Q\) and \(0 \leq w \leq 1\).

This implies that \(U\) is additive and it is also unique up to affine transformation.

Proof: If \(w\) is not unique then \(\exists w_1\) such that \(w_1 P + (1 - w_1 ) Q \sim R\). Without loss of generality assume that \(w_1 < w\) and so \(0 < w - w_1 < 1 - w_1\). However, we can write the bet \(Q\) as \[ Q = \left ( \frac{w-w_1}{1-w_1} \right ) Q + \left ( \frac{1-w}{1-w_1} \right ) Q \] By transitivity, as \(P \succeq Q\) we have \[ \left ( \frac{w-w_1}{1-w_1} \right ) P + \left ( \frac{1-w}{1-w_1} \right ) Q \succeq Q \] However, \[ w P + ( 1 - w) Q = w_1 P + (1 - w_1 ) \left ( \left ( \frac{w-w_1}{1-w_1} \right ) P + \left ( \frac{1-w}{1-w_1} \right ) Q \right ) \] implying by transitivity that \[ w P + (1 - w ) Q \succeq w_1 P + (1 - w_1 ) Q \] which is a contradiction.

This can be used together with the axioms to then prove the existence and uniqueness of a utility function.

Theorem 4.1 (Uniqueness of Utility) If \(V\) is any other function satisfying these results then \(V\) is an affine function of \(U\).

Proof. If \(\forall P , Q\) we have \(P \sim Q\), then define \(u(P) \equiv 0\). Hence suppose that there exists \(S \succ T\). Define \(U(S) =1\) and \(U(T)=0\). For any \(P \in \mathcal{P}\) there are five possibilities: \(P \succ T\) or \(P \sim S\) or \(S \succ P \succ T\) or \(P \sim T\) or \(T \succ P\).

In the first case define \(1/U(P)\) to be the unique \(p\) (see previous theorem) defined by \(p P + ( 1 -p )T \sim S\). In the second case, define \(U(P) =1\). In the third, there exists a unique \(q\) with \(q S + ( 1 -q )T \sim P\) and then define \(U(P)=q\). In the fourth case, define \(U(P)=0\) and finally when \(T \succ P\) there exists a unique \(r\) with \(r S + ( 1-r )P \sim T\) and then we define \(U(P) = - r / (1 - r)\).

Then check that \(U(P)\) satisfies the conditions. See Savage (1954), Ramsey (1927) and de Finetti (1931)

Other interesting extensions: how do people come to a consensus (DeGroot 1974; Morris 1994, 1996). Ramsey (1926) observation that if someone is willing to offer you a bet then that’s conditioning information for you. All probabilities are conditional probabilities.

If the bet outcome \(x\) is a monetary value, then the utility functions \(x, x^2, \sqrt{x}, \ln x\) are all monotonically increasing (the more the better). However, the utility function \(x^2\) is convex and the utility function \(\ln x\) is concave. The concavity of the utility function implies that the agent is risk averse and the convexity implies that the agent is risk seeking.

Example 4.1 (Saint Petersburg Paradox) The Saint Petersburg paradox is a concept in probability and decision theory that was first introduced by Daniel Bernoulli in 1738. It revolves around the idea of how individuals value risky propositions and how those valuations may not align with classical expected utility theory.

The paradox is named after the city of Saint Petersburg, where the problem was formulated. Here’s a simplified version of the paradox:

Imagine a gambling game where a fair coin is flipped repeatedly until it lands on heads. The payoff for the game is \(2^N\), where \(N\) is the number of tosses needed for the coin to land on heads. The expected value of this game, calculated by multiplying each possible payoff by its probability and summing the results, is infinite:

\[ E(X) = \frac{1}{2} \cdot 2 + \frac{1}{4} \cdot 4 + \frac{1}{8} \cdot 8 + \ldots = \infty \]

This means that, in theory, a rational person should be willing to pay any finite amount to play this game, as the expected value is infinite. However, in reality, most people would be unwilling to pay a large amount to play such a game.

The paradox arises because traditional expected utility theory assumes that individuals make decisions based on maximizing their expected gain. Bernoulli argued that people do not maximize expected monetary value but rather expected utility, where utility is a subjective measure of satisfaction or happiness. He proposed that individuals exhibit diminishing marginal utility for wealth, meaning that the additional satisfaction gained from an extra unit of wealth decreases as total wealth increases.

In the case of the Saint Petersburg paradox, although the expected monetary value is infinite, the utility gained from each additional dollar diminishes rapidly, leading to a reluctance to pay large amounts to play the game.

In modern decision theory and economics, concepts like diminishing marginal utility and expected utility are fundamental in understanding how individuals make choices under uncertainty and risk. The Saint Petersburg paradox highlights the limitations of relying solely on expected monetary value in explaining human behavior in such situations.

One common approach is to consider aspects of potential players, such as their possible risk aversion, available funds, etc., through a utility function \(U(x)\). Applying a utility function in this situation means changing our focus to the quantity \[ E[U(X)] = \sum^\infty_{k=1} 2^{-k} U(2^k). \]

Some examples of utility functions are,

- \(U(x) = W_0 (1-x^{-\alpha})\), \(\alpha > 0\), which gives an expected utility of \(W_0 \left(1-\frac{1}{2^{\alpha+1}-1}\right)\)

- Log utility, \(U(x) = \log(x)\), with expected value \(2 \log(2)\).

Notice that after obtaining an expected utility value, you’ll have to find the corresponding reward/dollar amount.

For the log utility case, we need to find the certain dollar amount \(x^*\) that provides the same utility as playing the game. Setting \(U(x^*) = 2\log(2)\), we solve: \[ \log(x^*) = 2\log(2) = \log(2^2) = \log(4) \] which gives \(x^* = 4\). Therefore, under log utility, a rational player would be willing to pay at most $4 to play the Saint Petersburg game, despite its infinite expected monetary value. This is a dramatic reduction from infinity and demonstrates how risk aversion (captured by the concave log utility function) resolves the paradox.

Similarly, for the power utility \(U(x) = W_0 (1-x^{-\alpha})\) with \(\alpha > 0\), we have an expected utility of \(W_0 \left(1-\frac{1}{2^{\alpha+1}-1}\right)\). To find the certainty equivalent \(x^*\), we solve: \[ W_0 (1-(x^*)^{-\alpha}) = W_0 \left(1-\frac{1}{2^{\alpha+1}-1}\right) \] which simplifies to \((x^*)^{-\alpha} = \frac{1}{2^{\alpha+1}-1}\), giving: \[ x^* = \left(2^{\alpha+1}-1\right)^{1/\alpha} \] For example, with \(\alpha = 1\), we get \(x^* = (2^2-1)^1 = 3\) dollars. As risk aversion increases (larger \(\alpha\)), the certainty equivalent further decreases.

Bernoulli’s resolution of this paradox was a watershed moment: it shifted the focus from objective expected value (which is infinite here) to subjective expected utility. This idea—that people value money non-linearly—became the cornerstone of the modern economic theory of risk.

Example 4.2 (Newcomb’s Problem) Newcomb’s problem, introduced by physicist William Newcomb and first analyzed philosophically by Robert Nozick in 1969, remains one of the most debated puzzles in decision theory. It exposes a fundamental tension between two seemingly reasonable principles for making decisions under uncertainty.

Following Seidenfeld (1984), the canonical formulation involves a choice between two options: option₁—to take the contents of an opaque box (one-box); and option₂—to take the contents of the opaque box plus the $1,000 in the transparent box (two-boxes). The opaque box contains either $1,000,000 or nothing, depending upon a demon’s earlier prediction that the choice is for one-box or for two-boxes. The decision matrix summarizes the choice problem:

| Demon predicts correctly | Demon predicts incorrectly | |

|---|---|---|

| Option₁ (one-box) | $1,000,000 | $0 |

| Option₂ (two-boxes) | $1,000 | $1,001,000 |

This Savage-styled formulation frames the demon’s accuracy as the state of the world. Seidenfeld notes the convenience: the verity of the demon’s prediction affords a binary partition of states that can be treated as probabilistically act-independent. What is striking is that neither option dominates the other—option₁ wins when the demon is correct, option 2 wins when incorrect. Yet taking two boxes always yields $1,000 more for any fixed content of the opaque box. We assume the agent takes no interest in the consequences apart from monetary outcomes (no intrinsic desire to frustrate the demon). The twist is to add a constraint that the chooser admits the demon is a very accurate predictor, with conditional probability given the agent’s choice: \[ P(\text{demon predicts option}_i \mid \text{option}_i) = 1 - \varepsilon \approx 1. \]

Then the conditional expected utility of option₁ exceeds that of option₂—against the recommendation afforded by appeal to dominance. As Seidenfeld notes, this exposes a “deep rooted problem in normative expected utility theory” arising from “the difference between probabilistic dependence and causal dependence across act-state pairs.”

Two principles from decision theory give conflicting advice:

Conditional Expected Utility: Given the predictor’s high accuracy, the expected value of one-boxing is approximately \((1-\varepsilon) \times 1{,}000{,}000 + \varepsilon \times 0 \approx \$1{,}000{,}000\), while two-boxing yields approximately \(\varepsilon \times 1{,}001{,}000 + (1-\varepsilon) \times 1{,}000 \approx \$1{,}000\). One-boxing maximizes expected utility.

Strategic Dominance: The predictor has already made the prediction and placed the money. Whatever is in the opaque box is “fixed and determined” when the agent chooses. Attention to the causal efficacy of the choice makes the dominating option right.

The limiting case illuminates the paradox. Consider an infallible demon where \(\varepsilon = 0\). Then by standard decision theory, the problem becomes one of choice under certainty—there is no risk involved. Taking option₁ and getting $1,000,000, or taking option₂ and getting $1,000, are the only possibilities. Do causal decision theorists advocate option₂ when it is certain to yield $1,000 whereas option₁ is certain to yield $1,000,000? As Seidenfeld argues, “To recommend two-boxes in this case is to contravene more than subjective expected utility theory—it is to overturn what is non-controversial by all standard accounts of choice, from expected utility to minimax theory to the very principle of dominance.”

Seidenfeld also raises a compelling third-person version: if your friend faces the Newcomb choice, what are your betting odds that conditional on option₁ your friend becomes a millionaire? By the weakest principles of conditionalization, these are fixed by the problem’s constraints. What is your fair-market price for your friend’s choice? Given your friend chooses one-box, is there any reason to pass up the bargain to buy the proceeds for $10,000?

The problem touches on deep questions about causation and free will. Causal decision theory holds that we should choose actions based on their causal consequences—and since our choice cannot causally affect what is already in the opaque box, we should two-box. Evidential decision theory counters that we should choose actions that provide the best evidence about outcomes—and one-boxing is strong evidence that the box contains the million.

Newcomb’s problem has practical relevance beyond philosophy. In game theory, similar structures arise when facing opponents who can anticipate your strategy. In artificial intelligence, it relates to how agents should reason when their decision procedures are transparent to other agents. The problem also connects to debates about deterrence in international relations, where the credibility of threats depends on whether adversaries believe you would follow through—a prediction about your future choice that influences present outcomes.

A 2020 survey of professional philosophers found a modest plurality (39% vs. 31%) favoring two-boxing, though the debate remains very much alive. The problem continues to generate new insights into the foundations of rational decision-making and the relationship between choice and causation.

Now, consider a more general situation, when you have two gambles 1: get \(P_1\) for sure, 2: get \(P_2 = P_1+k\) and \(P_3 = P_1-k\) with probability 1/2. Then we will compare the utility of those gambles \[ \dfrac{1}{2}U(P_2) + \dfrac{1}{2}U(P_3) \text{ and } U(P_1). \] If the utility function is linear then we should be indifferent between the two gambles. However, if the utility function is concave then we should prefer the sure thing. This is known as the certainty effect. \[ \dfrac{1}{2}U(P_2) + \dfrac{1}{2}U(P_3) < U(P_1). \]

The usual situation can be described as follows. Let \(\Omega\) be a finite set of possible outcomes with \(\Omega = \{ \omega_1 , \ldots , \omega_n \}\). Let \(P_i\) be the consequence that assigns one to outcome \(\omega_i\) and zero otherwise and let \(P = ( p_1 , \ldots , p_n )\) assign probability \(p_i\) to outcome \(\omega_i\). Then we can write the expected utility, \(U(P)\), of the gamble \(P\) as \[ U(P) = \sum_{i=1}^n p_i U( P_i ). \] That is, the utility of \(P\) is the expected value of a random variable \(W\) (wealth) that takes the value \(U(P_i)\) if the outcome is \(\omega_i\). Therefore, we can write \(U(P) = \mathbb{E}_P \left ( U( W ) \right)\).

This leads us to the notion of risk aversion and a categorization of agents according to their risk tolerance: the agent is said to be

- Risk Averse if \(\mathbb{E}_P \left ( U(W) \right ) \leq U \left ( \mathbb{E}_P (W) \right )\)

- Risk Neutral if \(\mathbb{E}_P \left ( U(W) \right ) = U \left ( \mathbb{E}_P (W) \right )\)

- Risk Seeking if \(\mathbb{E}_P \left ( U(W) \right ) \geq U \left ( \mathbb{E}_P (W) \right )\)

Here we assume that these hold for all probabilities and random variables. Risk aversion is equivalent to the agent having concave utility and risk seeking convex.

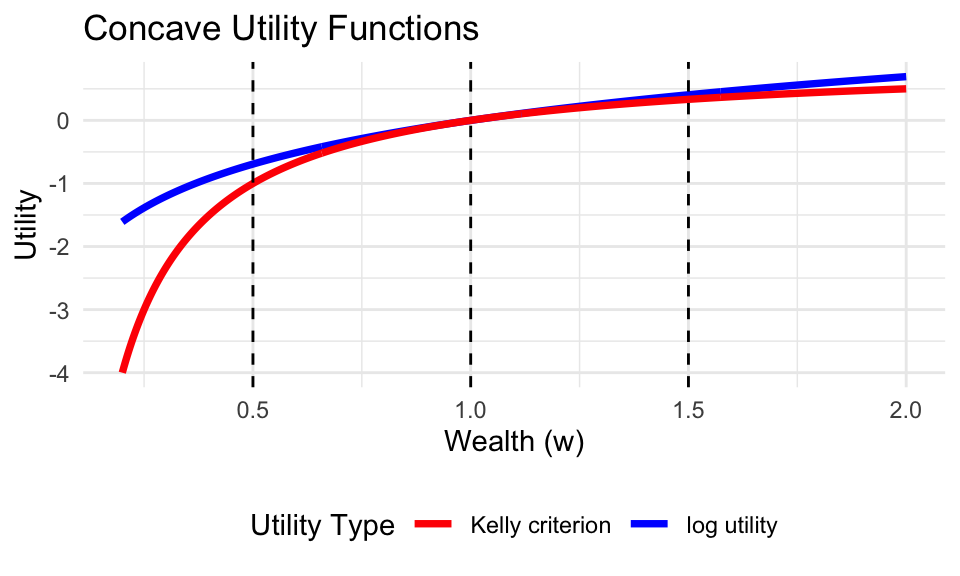

Example 4.3 (Risk Aversion) Consider the family of Constant Relative Risk Aversion (CRRA) utility functions. This family includes the log-utility (Kelly) \[ U(W)=\log(W), \] and the power utility \[ U(W)=\dfrac{W^{1-\gamma} - 1}{1-\gamma}. \] The log-utility is a limiting case of the power utility when \(\gamma \to 1\). The parameter \(\gamma\) controls the curvature of the function and is known as the coefficient of relative risk aversion: \[ R(W) = -W \frac{U''(W)}{U'(W)} = \gamma. \] Higher values of \(\gamma\) imply greater concavity, meaning the agent is more risk-averse and requires a higher risk premium to accept a gamble.

- \(\gamma \to 0\): Risk neutral (linear utility).

- \(\gamma = 0.5\): Moderate risk aversion (less than log).

- \(\gamma = 1\): Log utility (Kelly criterion).

- \(\gamma > 1\): High risk aversion (e.g., fractional Kelly).

Figure 4.1 demonstrates the effect of \(\gamma\). As \(\gamma\) increases, the utility function becomes more curved (“bends” more). This means that losses (moving left from \(W=1\)) hurt much more in utility terms than equivalent gains (moving right) help.

To see this concretely, consider a simple gamble with two equally likely outcomes: wealth \(w_1 = 0.5\) and \(w_2 = 1.5\). The expected wealth is \(E[W] = 0.5(0.5) + 0.5(1.5) = 1.0\).

For a risk-neutral agent (\(\gamma=0\)), the utility is linear, so the value of the gamble is exactly the expected wealth (\(1.0\)). However, for a risk-averse agent (\(\gamma > 0\)), the utility of the expected wealth is greater than the expected utility of the gamble. The Certainty Equivalent (CE) is the guaranteed amount of wealth that provides the same utility as the risky gamble. The difference between the expected wealth and the certainty equivalent is the Risk Premium—the amount the agent is willing to “pay” (forgo in expected value) to avoid the risk.

The table below shows how the Certainty Equivalent decreases and the Risk Premium increases as the risk aversion parameter \(\gamma\) grows.

| Risk Aversion (\(\gamma\)) | Certainty Equivalent | Risk Premium |

|---|---|---|

| 0.0 | 1.00 | 0.000 |

| 0.5 | 0.93 | 0.067 |

| 1.0 | 0.87 | 0.134 |

| 2.0 | 0.75 | 0.250 |

| 4.0 | 0.62 | 0.378 |

Example 4.4 (Kelly Criterion) The Kelly criterion has been used effectively by many practitioners. Ed Thorp, in his book Beat the Dealer, pioneered its use in blackjack and later applied it to investing in financial markets. Since then, many market participants, such as Jim Simons, have stressed the importance of this money management approach. The criterion’s application extends to other domains: Phil Laak described its use for bet sizing in a game-theoretic approach to poker, and Bill Benter applied it to horse racing. Stewart Ethier provided a mathematical framework for multiple outcomes and analyzed a “play the winner” rule in roulette. Claude Shannon also developed a system to detect and exploit unintentionally biased roulette wheels, an endeavor chronicled in the book The Eudaemonic Pie.

Suppose you have $1000 to invest. With probability \(0.55\) you will win whatever you wager and with probability \(0.45\) you lose whatever you wager. What’s the proportion of capital that leads to the fastest compounded growth rate?

Quoting Kelly (1956), the exponential rate of growth, \(G\), of a gambler’s capital is \[ G = \lim_{T\to \infty} \frac{1}{T} \log_2 \frac{W_T}{W_0} \] for initial capital \(W_0\) and capital after \(T\) bets \(W_T\).

Under the assumption that a gambler bets a fraction of his capital, \(\omega\), each time, we use \[ W_T = (1+\omega)^W (1-\omega)^L W_0 \] where \(W\) and \(L\) are the number of wins and losses in \(N\) bets. We get \[ G = p \log_2(1+\omega)+ q \log_2(1-\omega) \] in which the limit(s) of \(\frac{W}{N}\) and \(\frac{L}{N}\) are the probabilities \(p\) and \(q\), respectively.

This also comes about by considering the sequence of i.i.d. bets with \[ p ( X_t = 1 ) = p \; \; \text{ and} \; \; p ( X_t = -1 ) = q=1-p \] We want to find an optimal allocation \(\omega^*\) that maximizes the expected long-run growth rate: \[\begin{align*} \max_\omega \mathbb{E} \left ( \ln ( 1 + \omega W_T ) \right ) & = p \ln ( 1 + \omega ) + (1 -p) \ln (1 - \omega ) \\ & \leq p \ln p + q \ln q + \ln 2 \; \text{ and} \; \omega^\star = p - q \end{align*}\]

The solution is \(w^* = 0.55 - 0.45 = 0.1\).

Both approaches give the same optimization problem, which, when solved, give the optimal fraction rate \(\omega^* = p-q\), thus, with \(p=0.55\), the optimal allocation is 10% of capital.

We can generalize the rule to the case of asymmetric payouts \((a,b)\). Then the expected utility function is \[ p \ln ( 1 + b \omega ) + (1 -p) \ln (1 - a \omega ) \] The optimal solution is \[ \omega^\star = \frac{bp - a q}{ab} \]

If \(a=b=1\) this reduces to the pure Kelly criterion.

A common case occurs when \(a=1\) and market odds \(b=O\). The rule becomes \[ \omega^* = \frac{p \cdot O -q }{O}. \]

Let’s consider another scenario. You have two possible market opportunities: one where it offers you \(4/1\) when you have personal odds of \(3/1\) and a second one when it offers you \(12/1\) while you think the odds are \(9/1\).

In expected return these two scenarios are identical both offering a 33% gain. In terms of maximizing long-run growth, however, they are not identical.

Table 4.1 shows the Kelly criterion advises an allocation that is twice as much capital to the lower odds proposition: \(1/16\) weight versus \(1/40\).

| Market | You | \(\Delta\) | \(\omega^\star\) |

|---|---|---|---|

| \(4/1\) | \(3/1\) | \(1/4\) | \(1/16\) |

| \(12/1\) | \(9/1\) | \(1/10\) | \(1/40\) |

The optimal allocation \(\omega^\star = ( p O - q ) / O\) is \[ \frac{ (1/4) \times 4 - (3/4) }{4} = \frac{1}{16} \; \text{ and} \; \frac{ (1/10) \times 12 - (9/10) }{12} = \frac{1}{40}. \]

Note, that although the expected return is the same, the risk is different. The first gamble has a higher variance than the second gamble.

Example 4.5 (Kelly Criterion for Long-Term Investing) The following example is adapted from Thorp (2011). In 1964, a young hedge fund manager acquired a substantial interest in a small New England textile company called Berkshire Hathaway. The stock traded then at 20. In 1998 it traded at 70,000, a multiple of 3500, and an annualized compound growth rate of about 27%, or an instantaneous rate of 24%. The once-young hedge fund manager Warren Buffett is now acknowledged as the greatest investor of our time, and the world’s second richest man. You may read about Buffett in Lowenstein (1997), Hagstrom (1994), Kilpatrick (1994), and Lowenstein (1995). If, as I was, you were fortunate enough to meet Buffett and identify the Berkshire opportunity, what strategy does our method suggest?

Assume the drift rate \(m = 0.20\), \(s = 0.15\), \(r = 0.06\). Note: plausible arguments for a smaller future drift rate include regression towards the mean, the increasing size of Berkshire, and risk from the aging of management. A counter-argument is that Berkshire’s compounding rate has been as high in its later years as in its earlier years. However, the S&P 500 Index has performed much better in recent years so the spread between the growth rates of the Index and of Berkshire has been somewhat less. So, if we expect the Index growth rate to revert towards the historical mean, then we expect Berkshire to do so even more.

From the Kelly criterion formulas, we obtain: \[ f^* = 6.22, \quad g_\infty(f^*) = 0.495, \quad \text{Sdev}(G_\infty(f^*)) = 0.93, \] \[ tg_\infty(f^*) = 1.76k^2, \quad t = 3.54k^2 \text{ years}. \]

Compare this to the unlevered portfolio, where \(f = 1\) and \(c = 1/6.22 \approx 0.1607\). We find: \[ f = 1, \quad g_\infty(f) = 0.189, \quad \text{Sdev}(G_\infty(f)) = 0.15, \] \[ tg_\infty(f) = 0.119k^2, \quad t_k = 0.63k^2 \text{ years}. \]

Leverage to the level \(6.22\) would be inadvisable here in the real world because security prices may change suddenly and discontinuously. In the crash of October 1987, the S&P 500 index dropped 23% in a single day. If this happened at leverage of 2.0, the new leverage would suddenly be \(77/27 = 2.85\) before readjustment by selling part of the portfolio. In the case of Berkshire, which is a large well-diversified portfolio, suppose we chose the conservative \(f = 2.0\). Note that this is the maximum initial leverage allowed “customers” under current regulations.

Then \(g_\infty(2) = 0.295\). The values in 30 years for median \(V_\infty/V_0\) are approximately: \(f = 1\), \(V_\infty/V_0 = 288\); \(f = 2\), \(V_\infty/V_0 = 6,974\); \(f = 6.22\), \(V_\infty/V_0 = 2.86 \times 10^6\). So the differences in results of leveraging are enormous in a generation.

The results of Section 3 apply directly to this continuous approximation model of a (possibly) leveraged securities portfolio. The reason is that both involve the same “dynamics”, namely \(\log G_\alpha(f)\) is approximated as (scaled) Brownian motion with drift. So we can answer the same questions here for our portfolio that were answered in Section 3 for casino betting. For instance \((3.2)\) becomes \[ \text{Prob}(V(t)/V_0 \leq x \text{ for some } t) = x^{\wedge}(2g_\infty/\text{Var}(G_\infty)) \] where \(\wedge\) means exponentiation and using \((7.4)\), for \(r = 0\) and \(f = f^*\), \(2g_\infty/\text{Var}(G_\infty) = 1\) so that \(\text{Prob}(\cdot) = x\).

Power utility and log-utilities allow us to model constant relative risk aversion (CRRA). The main advantage is that the optimal rule is unaffected by wealth effects. The CRRA utility of wealth takes the form \[ U_\gamma (W) = \frac{ W^{1-\gamma} -1 }{1-\gamma} \]

The special case \(U(W) = \log (W )\) for \(\gamma = 1\). This leads to a myopic Kelly criterion rule.

4.2 Historical Perspectives on Optimal Decision Making

The principles of optimal decision-making under uncertainty have deep historical roots that extend well beyond modern portfolio theory. Understanding this intellectual lineage enriches our appreciation of the Kelly criterion and provides important lessons about risk management.

De Finetti’s Insurance Problem

In 1940, more than a decade before the canonical papers on portfolio theory, the Italian mathematician Bruno de Finetti addressed the problem of optimal retention in insurance (de Finetti 1940). An insurance company holding a portfolio of policies faces a crucial decision: how much of each policy’s risk should it retain versus reinsuring? This is essentially an asset allocation problem where the “assets” are insurance policies with uncertain payouts.

De Finetti formulated this as a mean-variance optimization problem with constraints \(0 \le f_i \le 1\) on the retention fractions, where \(f_i\) represents the fraction of policy \(i\) kept for the company’s own account. For uncorrelated risks, he proved that the optimal retention for each policy should be \[ f_i = A \frac{k_i}{\sigma_i^2} \] where \(k_i\) is the margin of gain from the policy, \(\sigma_i^2\) is its variance, and \(A\) is a constant determined by the company’s risk tolerance. This elegant result states that retention should be proportional to profitability and inversely proportional to variance—precisely the Kelly criterion’s risk-return trade-off.

Remarkably, de Finetti extended this analysis to the case of correlated risks, recognizing that insurance claims (like stock returns) are often positively correlated due to common factors such as economic conditions or natural disasters. In this case, the problem becomes significantly more complex. De Finetti showed that with correlations, one must solve a system of linear equations to determine optimal retentions, and he outlined—though did not fully solve—the general algorithm for finding the efficient frontier when risks are correlated.

De Finetti also introduced what we now call the “index of stability” for the long-run solvency of an insurance company. If \(G\) is the guarantee fund, \(m\) the expected annual gain, and \(\sigma^2\) the variance of gains, then the probability of ruin \(P\) over the long run is approximately \[ P \approx e^{-\xi} \quad \text{where} \quad \xi = \frac{2mG}{\sigma^2} \] This shows that stability increases linearly with the profit margin and capital reserves, but decreases with the square of risk—a fundamental relationship that applies equally to trading and investment.

Markowitz’s Recognition

It was not until 2006 that Harry Markowitz, in a paper titled “De Finetti Scoops Markowitz” (Markowitz 2006), brought widespread attention to de Finetti’s pioneering work. Markowitz acknowledged that de Finetti had essentially proposed mean-variance analysis with correlated risks in 1940, more than a decade before the famous 1952 papers by Markowitz himself and A.D. Roy.

Despite their mathematical similarity, the two formulations differ in important ways that reflect their distinct applications. Markowitz’s portfolio problem includes a budget constraint \(\sum X_i = 1\) (fractions invested must sum to one) and seeks either to maximize expected return for a given level of variance, or equivalently to minimize variance for a given expected return. In contrast, de Finetti’s reinsurance problem has no budget constraint—the company can choose any retention fractions \(0 \le f_i \le 1\) independently for each policy. His objective is to minimize risk (variance) subject to maintaining a fixed level of expected profit from the portfolio. Both formulations trace out an efficient frontier, but they arrive there from different starting points: Markowitz optimizes the trade-off between return and risk along a budget line, while de Finetti optimizes retention to minimize risk for a desired profit margin. Mathematically, both can be solved by minimizing \(L = \frac{1}{2}V_P - w E_P\) for various weights \(w\), but the constraint sets differ fundamentally.

Markowitz noted that while de Finetti solved the reinsurance problem completely for uncorrelated risks and outlined key properties for the correlated case, he did not provide a complete computational algorithm for the latter. Markowitz showed that the de Finetti problem is a special case of problems solvable by the Critical Line Algorithm (CLA) he developed in 1956. The CLA efficiently traces out the entire efficient frontier by moving along connected line segments in \((X, \eta, \lambda)\) space, where \(\eta_i = \partial L/\partial X_i\) measures the marginal change in the objective function.

An interesting feature of the de Finetti problem, which Markowitz corrected, concerns the final segment of the efficient frontier. De Finetti conjectured that the path from maximum expected return to minimum variance always approaches the zero portfolio from the interior of the feasible region. Markowitz proved this is not always true—with correlated risks, some policies may already be at zero retention on the final segment. However, Markowitz established a “correct last segment theorem”: once no policy is fully retained (all \(X_i < 1\)), that segment must lead directly to the minimum variance portfolio.

Dynamic Kelly and Bellman’s Principle

While the static Kelly criterion provides optimal allocation for a single period, real investors face sequential decisions where today’s choices affect tomorrow’s opportunities. This is where dynamic programming enters the picture. Richard Bellman’s Principle of Optimality (1957) states that “whatever the initial state and initial decision, the remaining decisions must constitute an optimal policy with regard to the state resulting from the first decision.”

For asset allocation, this leads to a fundamental recursion. If \(Q_t(s, a)\) denotes the value of taking action \(a\) in state \(s\) at time \(t\), then \[ Q_t(s, a) = \mathbb{E}[r(a, s, S_{t+1}) + V(S_{t+1}) \mid s, a] \] where \(V(s) = \max_a Q_t(s, a)\) is the value function. In the i.i.d. case with logarithmic utility, the myopic Kelly rule remains optimal—future learning opportunities don’t change today’s allocation. This remarkable simplification explains the Kelly criterion’s enduring popularity.

However, when the investor can learn about the underlying probabilities, the dynamic problem becomes more sophisticated (Jacquier and Polson 2013). Consider a Bernoulli-Beta setting where success probability \(p\) is unknown and the investor starts with prior \(p \sim \text{Beta}(\alpha, \beta)\). The myopic Kelly rule would invest nothing if \(\alpha < \beta\) (unfavorable prior odds). Yet the dynamic Bellman solution shows that even a risk-averse investor with \(\alpha < \beta\) should invest a small positive amount!

The reason is the option value of learning: by investing even when current odds seem unfavorable, the investor gains information that may reveal the true environment is actually favorable. For instance, with a uniform prior \(\text{Beta}(1,1)\) and 10 remaining periods, an investor might optimally allocate 11.7% even after observing one failure (giving posterior \(\text{Beta}(1,2)\) with expected odds 1:2 against). The potential to learn trumps the current negative expectation. This insight has profound implications for exploration-exploitation trade-offs in uncertain environments.

Livermore’s Trading Wisdom

The legendary trader Jesse Livermore, whose methods were chronicled in the 1923 classic Reminiscences of a Stock Operator, articulated trading principles that align remarkably well with Bellman’s optimal control framework (Polson and Witte 2014). Two of his famous maxims are particularly revealing:

“Profits always take care of themselves, but losses never do.” In the Bellman framework, suppose an investor holds a long position because \(Q_t(s, a_L) > Q_t(s, a_N)\) (long is better than neutral). If the position subsequently loses money, the trader faces a choice. Under unchanged beliefs, the same logic would suggest staying long. But Livermore’s insight is that the price movement itself contains information. By Bayes’ theorem, observing a loss should update beliefs such that \(Q_{t+1}^{q \cup \{x_t\}}(s', a_L) < Q_{t+1}^{q \cup \{x_t\}}(s', a_N)\), where \(q \cup \{x_t\}\) represents updated beliefs incorporating the price change. The optimal action is to exit. Conversely, a winning position confirms the original thesis—“it takes care of itself.”

“Never average down.” The practice of doubling up on losing positions seems to violate basic decision theory. If averaging down is optimal, it means \(Q_t(s', a_L) > Q_t(s', a_N)\) after a loss. But if we’ve updated beliefs based on the adverse price movement, this typically cannot hold unless we’ve received external information beyond what the market revealed. Livermore put it bluntly: “Why send good money after bad?”

These trading heuristics embody Bellman’s principle that the only thing that matters for optimal decision-making is the current state and what’s optimal going forward—not what you paid, what you hoped for, or what you “should” have made. The past is irrelevant except insofar as it informs beliefs about the future. This perspective removes emotional obstacles to sound decision-making: the sunk cost of past losses, the pride in being “right,” or the fear of admitting error.

These four contributions—de Finetti’s insurance mathematics, Markowitz’s portfolio theory, Bellman’s dynamic programming, and Livermore’s practical wisdom—represent complementary perspectives on the same fundamental problem of optimal decision-making under uncertainty. De Finetti provided the mathematical foundation showing that mean-variance optimization with betting constraints yields the Kelly-type allocation rules. Markowitz extended and formalized these methods, showing how to efficiently compute solutions even with correlations. Bellman revealed when and why sequential decision problems allow or forbid simple myopic solutions. And Livermore demonstrated that these theoretical principles have practical and timeless value in actual markets.

The common thread: optimal allocation depends on the ratio of expected excess return to variance, must account for correlations, must adapt to new information, and should never let past outcomes cloud judgment about future prospects. Whether managing an insurance portfolio in 1940, building an investment strategy in 1952, or trading in markets today, these principles remain the bedrock of rational decision-making.

4.3 Statistical Decisions and Risk

While Bernoulli’s work laid the foundation for expected utility, it was in the mid-20th century that L.J. Savage and John von Neumann/Oskar Morgenstern formalized these concepts into a rigorous mathematical decision theory. This framework provides the “rational” standard against which human behavior is often measured.

The statistical decision making problem can be posed as follows. A decision maker (you) has to choose from a set of decisions or acts. The consequences of these decisions depend on an unknown state of the world. Let \(d\in\mathcal{D}\) denote the decision and \(\theta\in\Theta\) the state of the world. As an example, think of \(\theta\) as the unknown parameter and the decision as choosing a parameter estimation or hypothesis testing procedure. To provide information about the parameter, the decision maker obtains a sample \(y\in\mathcal{Y}\) that is generated from the likelihood function \(p\left(y|\theta\right)\). The resulting decision depends on the observed data, is denoted as \(d\left( y\right)\), and is commonly called the decision rule.

To make the decision, the decision maker uses a “loss” function as a quantitative metric to assesses the consequences or performance of different decisions. For each state of the world \(\theta\), and decision \(d\), \(\mathcal{L}\left( \theta,d\right)\) quantifies the “loss” made by choosing \(d\) when the state of the world is \(\theta.\) Common loss functions include a quadratic loss, \(\mathcal{L}(\theta,d)=(\theta-d)^{2},\) an absolute loss, \(\mathcal{L}(\theta,d)=|\theta-d|\), and a \(0-1\) loss, \[ \mathcal{L}(\theta,d)=L_{0}1_{\left[ \theta\in\Theta_{0}\right] }+L_{1}1_{\left[ \theta\in\Theta_{1}\right] }. \] For Bayesians, the utility function provides a natural loss function. Historically, decision theory was developed by classical statisticians, thus the development in terms of “objective” loss functions instead of “subjective” utility.

Classical decision theory takes a frequentist approach, treating parameters as “fixed but unknown” and evaluating decisions based on their population properties. Intuitively, this thought experiment entails drawing a dataset \(y\) of given length and applying the same decision rule in a large number of repeated trials and averaging the resulting loss across those hypothetical samples. Formally, the classical risk function is defined as \[ R(\theta,d)=\int_{\mathcal{Y}}\mathcal{L}\left[ \theta,d(y)\right] p(y|\theta )dy=\mathbb{E}\left[ \mathcal{L}\left[ \theta,d(y)\right] |\theta\right] . \] Since the risk function integrates over the data, it does not depend on a given observed sample and is therefore an ex-ante or a-priori metric. In the case of quadratic loss, the risk function is the mean-squared error (MSE) and is \[\begin{align*} R(\theta,d) & =\int_{\mathcal{Y}}\left[ \theta-d\left( y\right) \right] ^{2}p(y|\theta)dy\\ & =\mathbb{E}\left[ \left( d\left( y\right) -E\left[ d\left( y\right) |\theta\right] \right) ^{2}|\theta\right] +\mathbb{E}\left[ \left( E\left[ d\left( y\right) |\theta\right] -\theta\right) ^{2}|\theta\right] \\ & =Var\left( d\left( y\right) |\theta\right) +\left[ bias\left( d\left( y\right) -\theta\right) \right] ^{2}% \end{align*}\] which can be interpreted as the bias of the decision/estimator plus the variance of the decision/estimator. Common frequentist estimators choose unbiased estimators so that the bias term is zero, which in most settings leads to unique estimators.

The goal of the decision maker is to minimize risk. Unfortunately, rarely is there a decision that minimizes risk uniformly for all parameter values. To see this, consider a simple example of \(y\sim N\left( \theta,1\right)\), a quadratic loss, and two decision rules, \(d_{1}\left( y\right) =0\) or \(d_{2}\left( y\right) =y\). Then, \(R\left( \theta,d_{1}\right) =\theta^{2}\) and \(R\left( \theta,d_{2}\right) =1\). If \(\left\vert \theta\right\vert <1\), then \(R\left( \theta,d_{1}\right) <R\left( \theta,d_{2}\right)\), with the ordering reversed for \(\left\vert \theta\right\vert >1\). Thus, neither rule uniformly dominates the other.

One way to deal with the lack of uniform domination is to use the minimax principle: first maximize risk as function of \(\theta\), \[

\theta^{\ast}=\underset{\theta\in\Theta}{\arg\max}R(\theta,d)\text{,}%

\] and then minimize the resulting risk by choosing a decision:

\[

d_{m}^{\ast}=\underset{d\in\mathcal{D}}{\arg\min}\left[ R(\theta^{\ast },d)\right] \text{.}%

\] The resulting decision is known as a minimax decision rule. The motivation for minimax is game theory, with the idea that the statistician chooses the best decision rule against the other player, mother nature, who chooses the worst parameter.

The Bayesian approach treats parameters as random and specifies both a likelihood and prior distribution, denoted here by \(\pi\left( \theta\right)\). The Bayesian decision maker recognizes that both the data and parameters are random, and accounts for both sources of uncertainty when calculating risk. The Bayes risk is defined as

\[\begin{align*}

r(\pi,d) & =\int_{\mathcal{\Theta}}\int_{\mathcal{Y}}\mathcal{L}\left[ \theta ,d(y)\right] p(y|\theta)\pi\left( \theta\right) dyd\theta\\

& =\int_{\mathcal{\Theta}}R(\theta,d)\pi\left( \theta\right) d\theta =\mathbb{E}_{\pi}\left[ R(\theta,d)\right] ,

\end{align*}\] and thus the Bayes risk is an average of the classical risk, with the expectation taken under the prior distribution. The Bayes decision rule minimizes expected risk:

\[

d_{\pi}^{\ast}=\underset{d\in\mathcal{D}}{\arg\min}\text{ }r(\pi,d)\text{.}%

\] The classical risk of a Bayes decision rule is defined as \(R\left(

\theta,d_{\pi}^{\ast}\right)\), where \(d_{\pi}^{\ast}\) does not depend on \(\theta\) or \(y\). Minimizing expected risk is consistent with maximizing posterior expected utility or, in this case, minimizing expected loss. Expected posterior risk is \[

r(\pi,d)=\int_{\mathcal{Y}}\left[ \int_{\mathcal{\Theta}}\mathcal{L}\left[

\theta,d(y)\right] p(y|\theta)\pi\left( \theta\right) d\theta\right] dy,

\] where the term in the brackets is posterior expected loss. Minimizing posterior expected loss for every \(y\in\mathcal{Y},\) is clearly equivalent to minimizing posterior expected risk, provided it is possibility to interchange the order of integration.

The previous definitions did not explicitly state that the prior distribution was proper, that is, that \(\int_{\mathcal{\Theta}}\pi\left( \theta\right)d\theta=1\). In some applications and for some parameters, researchers may use priors that do not integrate, \(\int_{\Theta}\pi\left( \theta\right)d\theta=\infty\), commonly called improper priors. A generalized Bayes rule is one that minimizes \(r(\pi,d),\) where \(\pi\) is not necessarily a distribution, if such a rule exists. If \(r(\pi,d)<\infty\), then the mechanics of this rule is clear, although its meaning is less clear.

4.4 Unintuitive Nature of Decision Making

Despite the elegant mathematical framework of Utility Theory and Statistical Decision Theory established by Savage and von Neumann, actual human decision-making often deviates from these normative axioms. Experiments by Ellsberg and Allais demonstrated that people frequently violate the axioms of independence and consistency when faced with ambiguity or specific risk profiles.

Example 4.6 (Ellsberg Paradox: Ambiguity Aversion) The Ellsberg paradox is a thought experiment that was first proposed by Daniel Ellsberg in 1961. It is a classic example of a situation where individuals exhibit ambiguity aversion, meaning that they prefer known risks over unknown risks. The paradox highlights the importance of considering ambiguity when making decisions under uncertainty.

There are two urns each containing 100 balls. It is known that urn A contains 50 red and 50 black, but urn B contains an unknown mix of red and black balls. The following bets are offered to a participant:

| Bet | Condition | Payoff if True | Payoff if False |

|---|---|---|---|

| 1A | Red drawn from urn A | $1 | $0 |

| 2A | Black drawn from urn A | $1 | $0 |

| 1B | Red drawn from urn B | $1 | $0 |

| 2B | Black drawn from urn B | $1 | $0 |

Most participants prefer bet 1A over 1B (preferring the known 50% chance over the unknown probability of drawing red from urn B), and they also prefer bet 2A over 2B (again preferring the known 50% chance over the unknown probability of drawing black from urn B).

This pattern of preferences violates the axioms of expected utility theory. If we denote the probability of drawing a red ball from urn B as \(p\), then:

- Preferring 1A over 1B implies: \(0.5 > p\)

- Preferring 2A over 2B implies: \(0.5 > (1-p)\), which means \(p > 0.5\)

These two inequalities are contradictory, yet this preference pattern is commonly observed. The paradox demonstrates that people exhibit ambiguity aversion: they prefer known probabilities (risk) over unknown probabilities (ambiguity), even when the expected values might be similar. This behavior cannot be explained by standard expected utility theory, which treats all probabilities symmetrically regardless of whether they are known or unknown.

The Ellsberg paradox has important implications for decision-making in real-world situations where probabilities are often ambiguous or unknown, such as in financial markets, insurance, or strategic business decisions. It vividly demonstrates that human decision-making is sensitive not just to risk (known probabilities) but to ambiguity (unknown probabilities). Standard expected utility theory fails to capture this “ambiguity aversion,” leading to the development of more generalized decision theories that incorporate confidence in probability estimates.

Example 4.7 (Allais Paradox: Independence Axiom) The Allais paradox is a choice problem designed by Maurice Allais to show an inconsistency of actual observed choices with the predictions of expected utility theory. The paradox is that the choices made in the second problem seem irrational, although they can be explained by the fact that the independence axiom of expected utility theory is violated.

We run two experiments. In each experiment a participant has to make a choice between two gambles.

Experiment 1

| Gamble \({\cal G}_1\) | Gamble \({\cal G}_2\) | ||

|---|---|---|---|

| Win | Chance | Win | Chance |

| $25m | 0 | $25m | 0.1 |

| $5m | 1 | $5m | 0.89 |

| $0m | 0 | $0m | 0.01 |

Experiment 2

| Gamble \({\cal G}_3\) | Gamble \({\cal G}_4\) | ||

|---|---|---|---|

| Win | Chance | Win | Chance |

| $25m | 0 | $25m | 0.1 |

| $5m | 0.11 | $5m | 0 |

| $0m | 0.89 | $0m | 0.9 |

The difference in expected gains is identical in two experiments

E1 <- 5 * 1

E2 <- 25 * 0.1 + 5 * 0.89 + 0 * 0.01

E3 <- 5 * 0.11 + 0 * 0.89

E4 <- 25 * 0.1 + 0 * 0.9

print(c(E1 - E2, E3 - E4))

## [1] -2 -2However, typically a person prefers \({\cal G}_1\) to \({\cal G}_2\) and \({\cal G}_4\) to \({\cal G}_3\), we can conclude that the expected utilities of the preferred are greater than the expected utilities of the second choices. The fact is that if \({\cal G}_1 \geq {\cal G}_2\) then \({\cal G}_3 \geq {\cal G}_4\) and vice-versa.

Assuming the subjective probabilities \(P = ( p_1 , p_2 , p_3)\). The expected utility \(E ( U | P )\) is \(u ( 0 ) = 0\) and for the high prize set \(u ( \$ 25 \; \text{million} ) = 1\), which leaves one free parameter \(u = u(\$ 5 \; \text{million})\).

Hence to compare gambles with probabilities \(P\) and \(Q\) we look at the difference \[ E ( u | P ) - E ( u | Q ) = ( p_2 - q_2 ) u + ( p_3 - q_3 ) \]

For comparing \({\cal G}_1\) and \({\cal G}_2\) we get \[\begin{align*} E ( u | {\cal G}_1 ) - E ( u | {\cal G}_2 ) &= 0.11 u - 0.1 \\ E ( u | {\cal G}_3 ) - E ( u | {\cal G}_4 ) &= 0.11 u - 0.1 \end{align*}\] The order is the same, given your \(u\). If your utility satisfies \(u < 0.1/0.11 = 0.909\) you take the “riskier” gamble.

The Allais paradox is particularly damaging to the Independence Axiom, which states that if you prefer A to B, you should also prefer A+C to B+C. Here, adding a common consequence flips the preference. This finding suggests that people value “certainty” disproportionately, a phenomenon famously captured by Prospect Theory.

Example 4.8 (Winner’s Curse) One of the interesting facts about expectation is that when you are in a competitive auctioning game then you shouldn’t value things based on pure expected value. You should take into consideration the event that you win \(W\). Really you should be calculating \(E(X\mid W)\) rather than \(E(X)\).

The winner’s curse: given that you win, you should feel regret: \(E(X\mid W) < E(X)\).

A good example is claiming racehorse whose value is uncertain.

| Value | Outcome |

|---|---|

| 0 | horse never wins |

| 50,000 | horse improves |

Simple expected value tells you \[ E(X) = \frac{1}{2} \cdot 0 + \frac{1}{2} \cdot 50,000 = \$25,000. \] In a $20,000 claiming race (you can buy the horse for this fixed fee ahead of time from the owner) it looks like a simple decision to claim the horse.

It’s not so simple! We need to calculate a conditional expectation. What’s \(E( X\mid W )\), given you win event (\(W\))? This is the expected value of the horse given that you win that is relevant to assessing your bid. In most situations \(E(X\mid W) < 20,000\).

Another related feature of this problem is asymmetric information. The owner or trainer of the horse may know something that you don’t know. There’s a reason why they are entering the horse into a claiming race in the first place.

Winner’s curse implies that immediately after you have won, you should feel a little regret, as the object is less valuable to you after you have won! Or put another way, in an auction nobody else in the room is willing to offer more than you at that time.

Example 4.9 (The Hat Problem) There are \(N\) prisoners in a forward facing line. Each guy is wearing a blue or red hat. Everyone can see all the hats in front of him, but cannot see his own hat. The hats can be in any combination of red and blue, from all red to all blue and every combination in between. The first guy doesn’t know his own hat.

A guard is going to walk down the line, starting in the back, and ask each prisoner what color hat they have on. They can only answer “blue” or “red.” If they answer incorrectly, or say anything else, they will be shot dead on the spot. If they answer correctly, they will be set free. Each prisoner can hear all of the other prisoners’ responses, as well as any gunshots that indicate an incorrect response. They can remember all of this information.

There is a rule that all can agree to follow such that the first guy makes a choice (“My hat is …”) and everyone after that, including the last guy, will get their color right with probability \(1\).

Here is the strategy:

- The last prisoner (Prisoner 100) counts the number of blue hats among the 99 people in front of him.

- If he sees an even number of blue hats, he yells “Blue”. If odd, he yells “Red”. This yell conveys the parity of blue hats to everyone else.

- Prisoner 99 hears the yell. Now knowing the total parity of blue hats (for 1..99), he counts the blue hats he sees (on 1..98).

- If the total parity (from 100) matches the parity he sees, his own hat must be Red (contributing 0 to the count).

- If the parities differ, his own hat must be Blue (changing the parity).

- He yells his calculated color, saving himself and passing the parity information down to Prisoner 98.

- This induction continues, allowing every prisoner except the first to determine their hat color with certainty. The first prisoner survives with probability 0.5 (random guess that conveys the bit).

One hundred prisoners are too many to work with. Suppose there are two (1 and 2, where 2 is the back). Prisoner 2 sees prisoner 1. If he sees Blue, he yells “Red” (odd). Prisoner 1 hears “Red”, sees 0 blue hats (even). Mismatch -> Blue. This logic extends to any \(N\). By using parity, the group collectively solves the problem with only 1 bit of uncertainty for the entire group.

Example 4.10 (Lemon’s Problem) The lemon problem is an interesting conditional probability puzzle and is a classic example of asymmetric information in economics. It was first proposed by George Akerlof in his 1970 paper “The Market for Lemons: Quality Uncertainty and the Market Mechanism.” The problem highlights the importance of information in markets and how it can lead to adverse selection, where the quality of goods or services is lower than expected.

The basic tenet of the lemons principle is that low-value cars force high-value cars out of the market because of the asymmetrical information available to the buyer and seller of a used car. This is primarily due to the fact that a seller does not know what the true value of a used car is and, therefore, is not willing to pay a premium on the chance that the car might be a lemon. Premium-car sellers are not willing to sell below the premium price so this results in only lemons being sold.

Suppose that a dealer pays $20K for a car and wants to sell for $25K. Some cars on the market are Lemons. The dealer knows whether a car is a lemon. A lemon is only worth $5K. There is asymmetric information as the customer doesn’t know if the particular new car is a lemon. S/he estimates the probability of lemons on the road by using the observed frequency of lemons. We will consider two separate cases:

- Let’s first suppose only 10% of cars are lemons.

- We’ll then see what happens if 50% are lemons.

The question is how does the market clear (i.e. at what price do car’s sell). Or put another way does the customer buy the car and if so what price is agreed on? This is very similar to winner’s curse: when computing an expected value what conditioning information should I be taking into account?

In the case where the customer thinks that \(p=0.10\) of the car’s are lemons, they are willing to pay \[ E (X)= \frac{9}{10} \cdot 25 + \frac{1}{10} \cdot 5 = \$ 23 K \] This is greater than the initial $20 that the dealer paid. The car then sells at $23K \(<\) $25K.

Of course, the dealer is disappointed that there are lemons on the road as he is not achieving the full value – missing $2000. Therefore, they should try and persuade the customer its not a lemon by offering a warranty for example.

The more interesting case is when \(p=0.5\). The customer now values the car at \[ E (X) = \frac{1}{2} \cdot 25 + \frac{1}{2} \cdot 5 = \$ 15K \] This is lower than the $20K – the reservation price that the dealer would have for a good car. Now what type of car and at what price do they sell?

The key point in asymmetric information is that the customer must condition on the fact that if the dealer still wants to sell the car, the customer must update his probability of the type of the car. We already know that if the car is not a lemon, the dealer won’t sell under his initial cost of $20K. So at $15K he is only willing to sell a lemon. But then if the customer computes a conditional expectation \(E( X \mid \mathrm{Lemon})\) – conditioning on new information that the car is a lemon \(L\) we get the valuation \[ E ( X \mid L ) = 1 \cdot 5 = \$ 5K \] Therefore only lemons sell, at $ 5K, even if the dealer has a perfectly good car the customer is not willing to buy!

Again what should the dealer do? Try to raise the quality and decrease the frequency of lemons in the observable market. This type of modeling has all been used to understand credit markets and rationing in periods of loss of confidence.

Example 4.11 (Envelope Paradox) The envelope paradox is a thought experiment or puzzle related to decision-making under uncertainty. It is also known as the “exchange paradox” or the “two-envelope paradox.” The paradox highlights the importance of carefully considering the information available when making decisions under uncertainty and the potential pitfalls of making assumptions about unknown quantities.

A swami puts \(m\) dollars in one envelope and \(2 m\) in another. He hands on envelope to you and one to your opponent. The amounts are placed randomly and so there is a probability of \(\frac{1}{2}\) that you get either envelope.

You open your envelope and find \(x\) dollars. Let \(y\) be the amount in your opponent’s envelope. You know that \(y = \frac{1}{2} x\) or \(y = 2 x\). You are thinking about whether you should switch your opened envelope for the unopened envelope of your friend. It is tempting to do an expected value calculation as follows \[ E(y) = \frac{1}{2} \cdot \frac{1}{2} x + \frac{1}{2} \cdot 2 x = \frac{5}{4} x > x \] Therefore, it looks as if you should switch no matter what value of \(x\) you see. A consequence of this, following the logic of backwards induction, that even if you didn’t open your envelope that you would want to switch! Where’s the flaw in this argument?

This problem permits multiple interpretations, yet it serves as an excellent case study for distinguishing between frequentist and Bayesian reasoning. Rather than addressing every possible condition, we will focus on the most instructive cases. First, assume we are risk-neutral (note that we can simply substitute “money” with “utility” without loss of generality). We will compare frequentist vs. Bayesian, and open vs. closed envelope scenarios.

If I DO NOT look in my envelope, in this case, even from a frequentist viewpoint, we can find a fallacy in this naive expectation reasoning \(E[trade] = 5x/4\) . First, the right answer from a frequentist view is, loosely, as follows. If we switch the envelope, we can obtain \(m\) (when \(X = m\)) or lose \(m\) (when \(X = 2m\)) with the same probability \(1/2\). Thus, the value of a trade is zero, so that trading matters not for my expected wealth.

Instead, naive reasoning is confusing the property of variables \(X\) and \(m\), \(X\) is a random variable and \(m\) is a fixed parameter which is constant (again, from a frequentist viewpoint). By trading, we can obtain \(m\) or lose \(m\) with the same probability. Here, the former \(X=m\) is different from the latter \(X= 2m\). Thus, \(X \frac{1}{2} - \frac{X}{2} \frac{1}{2} = \frac{X}{4}\) is the wrong expected value of trading. On the other hand, from a bayesian view, since we have no information, we are indifferent to either trading or not.

The second scenario is if I do look in my envelope. As the Christensen & Utts (1992) article said, the classical view cannot provide a completely reasonable resolution to this case. It is just ignoring the information revealed. Also, the arbitrary decision rule introduced at the end of the paper or the extension of it commented by Ross (1996) are not the results of reasoning from a classical approach. However, the bayesian approach provides a systematic way of finding an optimal decision rule using the given information.

We can use the Bayes rule to update the probabilities of which envelope your opponent has! Assume \(p(m)\) of dollars to be placed in the envelope by the swami. Such an assumption then allows us to calculate an odds ratio \[ \frac{ p \left ( Y = \frac{1}{2} x \mid X = x \right ) }{ p \left ( Y = 2 x \mid X = x \right ) } \] concerning the likelihood of which envelope your opponent has.

Then, the expected value is given by \[ E(Y\mid X = x) = p \left ( Y = \frac{1}{2} x \mid X = x \right ) \cdot \frac{1}{2} x + p \left ( Y = 2 x \mid X = x \right ) \cdot 2 x \] and the condition \(E(Y \mid X = x) > x\) becomes a decision rule.

Let \(g(m)\) be the prior distribution of \(m\). Applying Bayes’ theorem, we have \[ p(m = x \mid X = x) = \frac{p(X = x \mid m = x) g(x)}{p(X = x)} = \frac{g(x)}{g(x)+g(x/2)}. \] Similarly, we have \[ p(m = x/2 \mid X = x) = \frac{p(X = x \mid m = x/2) g(x/2)}{p(X = x/2)} = \frac{g(x/2)}{g(x)+g(x/2)}. \] The Bayesian can now compute his expected winnings from the two actions. If he keeps the envelope he has, he wins \(x\) dollars. If he trades envelopes, he wins \(x/2\) if he currently has the envelope with \(2m\) dollars, i.e., if \(m = x/2\) and he wins \(2x\) if he currently has the envelope with \(m\) dollars, i.e., \(m = x\). His expected winnings from a trade are \[ E(W\mid Trade) = E(Y\mid X = x) = \frac{g(x/2)}{g(x)+g(x/2)} \frac{x}{2} + \frac{g(x)}{g(x)+g(x/2)} 2x. \] It is easily seen that when \(g(x/2) = 2g(x)\), \(E(W\mid Trade) = x\). Therefore, if \(g(x/2) > 2g(x)\) it is optimal to keep the envelope and if \(g(x/2) < 2g(x)\) it is optimal to trade envelopes. For example, if your prior distribution on \(m\) is exponential \(\lambda\), so that \(g(m) = \lambda e^{-\lambda m}\), then it is easily seen that it is optimal to keep your envelope if \(x > 2\log(2)/\lambda\).

The intuitive value of the expected winnings when trading envelopes was shown to be \(5x/4\). This value can be obtained by assuming that \(g(x)/[g(x) + g(x/2)] = 1/2\) for all \(x\). In particular, this implies that \(g(x) = g(x/2)\) for all x, i.e., \(g(x)\) is a constant function. In other words, the intuitive expected winnings assumes an improper “noninformative” uniform density on \([0, \infty)\). It is of interest to note that the improper noninformative prior for this problem gives a truly noninformative (maximum entropy) posterior distribution.

Most of the arguments in the Christensen & Utts (1992) paper are right, but there is one serious error in the article which is corrected in Bachman-Christensen-Utts (1996) and discussed in Brams & Kilgour (1995). The paper calculated the marginal density of \(X\) like below. \[\begin{align*} p(X = x) &= p(m = x)g(x) + p(2m = x)g(x/2) \\ &= \frac{1}{2} g(x) + \frac{1}{2} g(x/2) \end{align*}\] where \(g(x)\) is the prior distribution of \(m\). However, integrating \(p(X = x)\) with respect to \(x\) from \(0\) to \(\infty\) gives \(3/2\) instead of \(1\). In fact, their calculation of \(p(X = x)\) can hold only when the prior distribution \(g(x)\) is discrete and \(p(X = x)\), \(g(m)\), \(g(m/2)\) represent the probabilities that \(X = x\), \(m = m\), \(m = m/2\), respectively.

For the correct calculation of the continuous \(X\) case, one needs to properly transform the distribution. That can be done by remembering to include the Jacobian term alongside the transformed PDF, or by working with the CDF of \(X\) instead. The latter forces one to properly consider the transform, and we proceed with that method.

Let \(G(x)\) be the CDF of the prior distribution of \(m\) corresponding to \(g(x)\). \[\begin{align*} p(x < X \leq x+dx) &= p(m = x)dG(x)+ p(2m = x)dG(x/2) \\ &= \frac{1}{2} \left( dG(x)+ dG(x/2) \right) \end{align*}\] where \(g(x) = dG(x)/dx\). Now, the PDF of \(X\) is \[\begin{align*} f_X(x) &= \frac{d}{dx} p(x < X \leq x + dx) \\ &= \frac{1}{2} \left(g(x) + \frac{1}{2} g(x/2) \right) \end{align*}\] We have an additional \(1/2\) in the last term due to the chain rule, or the Jacobian in the change-in-variable formula. (Recall that when transforming a probability density \(f_X(x)\) to \(f_Y(y)\) where \(y=g(x)\), we must scale by \(|dx/dy|\) to preserve the total probability mass of 1). Therefore, the expected amount of a trade is \[\begin{align*} E(Y\mid X = x) &= \frac{x}{2} p(2m = x\mid X = x) + 2 x \, p(m = x\mid X = x) \\ &= \frac{x}{2} \frac{g(x)}{g(x) + g(x/2)/2} + 2 x \frac{g(x/2)/2}{g(x) + g(x/2)/2} \\ &= \frac{\frac{x}{2}g(x) + x g(x/2)}{g(x) + g(x/2)/2} \end{align*}\]

Thus, for the continuous case, trading is advantageous whenever \(g(x/2) < 4g(x)\), instead of the decision rule for the discrete case \(g(x/2) < 2g(x)\).

Now, think about which prior will give you the same decision rule as the frequentist result. In the discrete case, \(g(x)\) such that \(g(x/2) = 2g(x)\), and in the continuous case \(g(x)\) such that \(g(x/2) = 4g(x)\). However, both do not look like useful, non-informative priors. Therefore, the frequentist approach does not always equal the Bayes approach with a non-informative prior. At the moment you start to treat \(x\) as a given number, and consider \(p(m \mid X = x)\) (or \(p(Y \mid X = x)\)), you are thinking in a bayesian way, and need to understand the implications and assumptions in that context.

4.5 Decision Trees

Decision trees can effectively model and visualize conditional probabilities. They provide a structured way to break down complex scenarios into smaller, more manageable steps, allowing for clear calculations and interpretations of conditional probabilities.

Each node in a decision tree, including the root, represents an event or condition. The branches represent the possible outcomes of that condition. Along each branch, you’ll often see a probability. This is the chance of that outcome happening, given the condition at the node. As you move down the tree, you’re looking at more specific conditions and their probabilities. The leaves of the tree show the final probabilities of various outcomes, considering all the conditions along the path to that leaf. Thus, the probabilities of the leaves need to sum to 1.

Example 4.12 (Medical Testing) A patient goes to see a doctor. The doctor performs a test which is 95% sensitive – that is 95 percent of people who are sick test positive and 99% specific – that is 99 percent of the healthy people test negative. The doctor also knows that only 2 percent of the people in the country are sick. Now the question is: if the patient tests positive, what are the chances the patient is sick? The intuitive answer is 99 percent, but the correct answer is 66 percent.

Formally, we have two binary variables, \(D=1\) that indicates you have a disease and \(T=1\) that indicates that you test positive for it. The estimates we know already are given by \(P(D) = 0.02\), \(P(T\mid D) = 0.95\), and \(P(\bar T \mid \bar D) = 0.99\). Here we used shortcut notations, instead of writing \(P(D=1)\) we used \(P(D)\) and instead of \(P(D=0)\) we wrote \(P(\bar D)\).

Sometimes it is more intuitive to describe probabilities using a tree rather than tables. The tree below shows the conditional distribution of \(D\) and \(T\).

graph LR

D --0.02--> d1(D=1)

D --0.98--> d0(D=0)

d1--0.95-->t1(T=1)

d1 --0.05--> t0(T=0)

d0--0.01-->t10(T=1)

d0 --0.99--> t00(T=0)

The result is counter-intuitive. Let’s think about this intuitively. Rather than relying on Bayesian math to help us with this, let us consider another illustration. Imagine that the above story takes place in a small town, with \(1,000\) people. From the prior \(P(D)=0.02\), we know that 2 percent, or 20 people, are sick, and \(980\) are healthy. If we administer the test to everyone, the most probable result is that 19 of the 20 sick people test positive. Since the test has a 1 percent error rate, however, it is also probable that 9.8 of the healthy people test positive, we round it to 10.

Now if the doctor sends everyone who tests positive to the national hospital, there will be 10 healthy and 19 sick patients. If you meet one, even though you are armed with the information that the patient tested positive, there is only a 66 percent chance this person is sick.

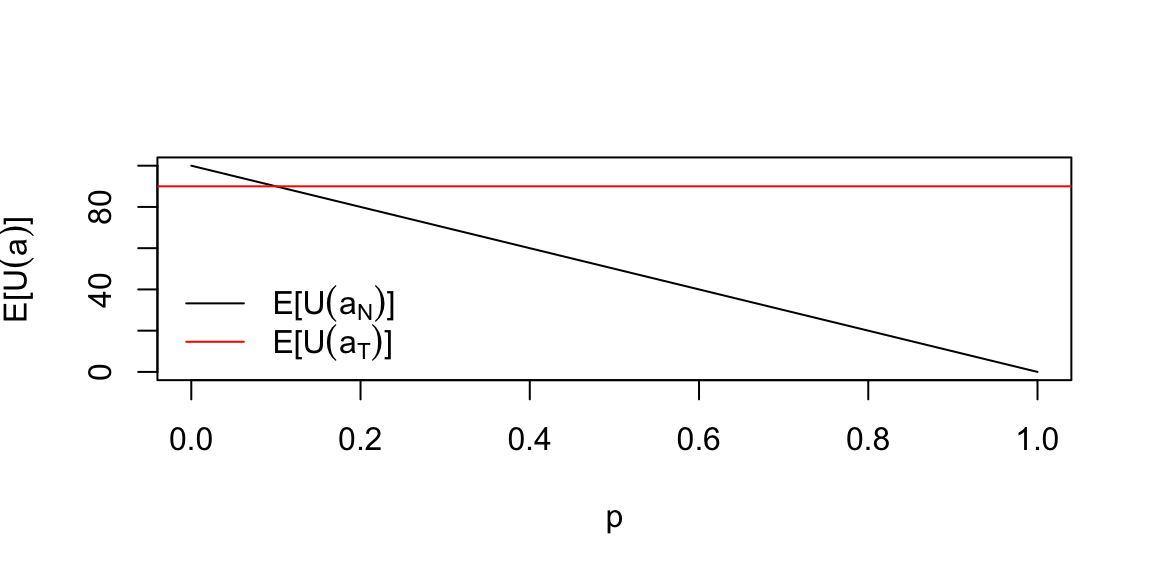

Let’s extend the example and add the utility of the test and the utility of the treatment. Then the decision problem is to treat \(a_T\) or not to treat \(a_N\). The Q-function is the function of the state \(S \in \{D_0,D_1\}\) and the action \(A \in \{a_T,a_N\}\)

| A/S | \(a_T\) | \(a_N\) |

|---|---|---|

| \(D_0\) | 90 | 100 |

| \(D_1\) | 90 | 0 |

Then expected utility of the treatment is 90 and no treatment is 98. A huge difference. Given our prior knowledge, we should not treat everyone.

0.02 * 90 + 0.98 * 90 # treat

## [1] 90

0.02 * 0 + (1 - 0.02) * 100 # do not treat

## [1] 98However, the expected utility will change when our probability of disease changes. Let’s say that we are in a country where the probability of disease is 0.1 or we performed a test and updated our prior probability of disease to some number \(p\). Then the expected utility of the treatment is \(E\left[U(a_T)\right] = 90\) and no treatment is \[ E\left[U(a_N)\right] = 0\cdot p + 100 \cdot (1-p) = 100(1-p) \] When we are unsure about the value of \(p\) we may want to explore how the optimal decision changes as we vary \(p\)

p <- seq(0, 1, 0.01)

plot(p, 100 * (1 - p), type = "l", xlab = "p", ylab = "E[U(a)]")

abline(h = 90, col = "red")

legend("bottomleft", legend = c(

TeX("$E[U(a_N)]$"),

TeX("$E[U(a_T)]$")

), col = c("black", "red"), lty = 1, bty = "n")

If our estimate is at the crossover point, then we should be indifferent between treatment and no treatment, if on the left of the crossover point, we should treat, and if on the right, we should not treat. The crossover point is. \[ 100(1-p) = 90, ~p = 0.1 \]

The gap of \(90-100(1-p)\) is the expected gain from treatment.

Now, let us calculate the value of test, e.g. the change in expected utility from the test. We will need to calculate the posterior probabilities

# P(D | T = 0) = P(T = 0 | D) P(D) / P(T = 0)

pdt0 <- 0.05 * 0.02 / (0.05 * 0.02 + 0.99 * 0.98)

# Expected utility given the test is negative

# E[U(a_N | T=0)]

UN0 <- pdt0 * 0 + (1 - pdt0) * 100

# E[U(a_T | T=0)]

UT0 <- pdt0 * 90 + (1 - pdt0) * 90

sprintf("P(D | T = 0) : %.4f, E[U(a_N | T=0)] : %.1f, E[U(a_T | T=0)] : %.1f", pdt0, UN0, UT0)

## [1] "P(D | T = 0) : 0.0010, E[U(a_N | T=0)] : 99.9, E[U(a_T | T=0)] : 90.0"Given test is negative, our best action is not to treat. Our utility is 100. What if the test is positive?

# P(D | T = 1) = P(T = 1 | D) P(D) / P(T = 1)

pdt <- 0.95 * 0.02 / (0.95 * 0.02 + 0.01 * 0.98)

# E[U(a_N | T=1)]

UN1 <- pdt * 0 + (1 - pdt) * 100

# E[U(a_T | T=1)]

UT1 <- pdt * 90 + (1 - pdt) * 90## [1] "P(D | T = 1) : 0.6597, E[U(a_N | T=1)] : 34.0, E[U(a_T | T=1)] : 90.0"The best option is to treat now! Given the test our strategy is to treat if the test is positive and not treat if the test is negative. Let’s calculate the expected utility of this strategy.

# P(T=1) = P(T=1 | D) P(D) + P(T=1 | D=0) P(D=0)

pt <- 0.95 * 0.02 + 0.01 * 0.98

# P(T=0) = P(T=0 | D) P(D) + P(T=0 | D=0) P(D=0)

pt0 <- 0.05 * 0.02 + 0.99 * 0.98

# Expected utility of the strategy

sprintf("P(T=1) : %.4f, P(T=0) : %.4f, E[U(a)] : %.1f", pt, pt0, pt * UT1 + pt0 * UN0)

## [1] "P(T=1) : 0.0288, P(T=0) : 0.9712, E[U(a)] : 99.6"The utility of our strategy of 100 is above the strategy prior to testing (98), this difference of 2 is called the value of information.

Example 4.13 (Mudslide) I live in a house that is at risk of being damaged by a mudslide. I can build a wall to protect it. The wall costs $10,000. If there is a mudslide, the wall will protect the house with probability \(0.95\). If there is no mudslide, the wall will not cause any damage. The prior probability of a mudslide is \(0.01\). If there is a mudslide and the wall does not protect the house, the damage will cost $100,000. Should I build the wall?

Let’s formally solve this as follows:

- Build a decision tree.

- The tree will list the probabilities at each node. It will also list any costs there are you going down a particular branch.

- Finally, it will list the expected cost of going down each branch, so we can see which one has the better risk/reward characteristics.

graph LR

B--"Build: $40, $40.5"-->Y

B--"Don't Build: $0, $10"-->N

Y--"Slide: $0, $90"-->yy[Y]

Y--"No slide $0, $40"-->40

N--"Slide: $1000, $1000"-->1000

N--"No slide $0, $0"-->0

yy --"Hold: $0, $40"-->401[40]

yy --"Not Hold: $1000, $1040"-->1040

The first dollar value is the cost of the edge, e.g. the cost of building the wall is $10,000. The second dollar value is the expected cost of going down that branch. For example, if you build the wall and there is a mudslide, the expected cost is $15,000. If you build the wall and there is no mudslide, the expected cost is $10,000. The expected cost of building the wall is $10,050. The expected cost of not building the wall is $1,000. The expected cost of building the wall is greater than the expected cost of not building the wall, so you should not build the wall. The dollar value at the leaf nodes is the expected cost of going down that branch. For example, if you build the wall and there is a mudslide and the wall does not hold, the expected cost is $110,000.

There’s also the possibility of a further test to see if the wall will hold. Let’s include the geological testing option. The test costs $3000 and has the following accuracies. \[ P( T \mid \mathrm{Slide} ) = 0.90 \; \; \mathrm{and } \; \; P( \mathrm{not~}T \mid \mathrm{No \; Slide} ) = 0.85 \] If you choose the test, then should you build the wall?

Let’s use the Bayes rule. The initial prior probabilities are \[ P( Slide ) = 0.01 \; \; \mathrm{and} \; \; P ( \mathrm{No \; Slide} ) = 0.99 \]

\[\begin{align*} P( T) & = P( T \mid \mathrm{Slide} ) P( \mathrm{Slide} ) + P( T \mid \mathrm{No \; Slide} ) P( \mathrm{No \; Slide} ) \\ P(T)& = 0.90 \times 0.01 + 0.15 \times 0.99 = 0.1575 \end{align*}\] We’ll use this to find our optimal course of action.

The posterior probability given a positive test is \[\begin{align*} P ( Slide \mid T ) & = \frac{ P ( T \mid Slide ) P ( Slide )}{P(T)} \\ & = \frac{ 0.90 \times 0.01}{ 0.1575} = 0.0571 \end{align*}\]

The posterior probability given a negative test is \[\begin{align*} P \left ( \mathrm{Slide} \mid \mathrm{not~}T \right ) & = \frac{ P ( \mathrm{not~}T \mid \mathrm{Slide} ) P ( \mathrm{Slide} )}{P(\mathrm{not~}T)} \\ & = \frac{0.1 \times 0.01 }{0.8425} \\ & =0.001187 \end{align*}\]

Compare this to the initial base rate of a \(1\)% chance of having a mud slide.

Given that you build the wall without testing, what is the probability that you’ll lose everything? With the given situation, there is one path (or sequence of events and decisions) that leads to losing everything:

- Build without testing (given) Slide (\(0.01\))

- Doesn’t hold (\(0.05\)) \[ P ( \mathrm{losing} \; \mathrm{everything} \mid \mathrm{build} \; \mathrm{w/o} \; \mathrm{testing} ) = 0.01 \times 0.05 = 0.0005 \]

Given that you choose the test, what is the probability that you’ll lose everything? There are two paths that lead to losing everything:

There are three things that have to happen to lose everything. Test +ve (\(P=0.1575\)), Build, Slide (\(P= 0.0571\)), Doesn’t Hold (\(P=0.05\))

Now you lose everything if Test -ve (\(P=0.8425\)), Don’t Build, Slide given negative (\(P=0.001187\)).

The conditional probabilities for the first path \[ P ( \mathrm{first} \; \mathrm{path} ) = 0.1575 \times 0.0571 \times 0.05 = 0.00045 \]

For the second path \[ P ( \mathrm{second} \; \mathrm{path} ) = 0.8425 \times 0.001187 = 0.00101 \]

Hence putting it all together \[ P ( \mathrm{losing} \; \mathrm{everything} \mid \mathrm{testing} ) = 0.00045 + 0.00101 = 0.00146 \]

Putting these three cases together we can build a risk/reward table

| Choice | Expected Cost | Risk | P |

|---|---|---|---|

| Don’t Build | $1,000 | 0.01 | 1 in 100 |

| Build w/o testing | $10,050 | 0.0005 | 1 in 2000 |

| Test | $4,693 | 0.00146 | 1 in 700 |

The expected cost with the test is \(3000+10000\times 0.1575+100000\times 0.001187 = 4693\)

What do you choose?

4.6 Nash Equilibrium

When multiple decision makers interact with each other, meaning the decision of one player changes the state of the “world” and thus affects the decision of another player, then we need to consider the notion of equilibrium. It is a central concept in economics and game theory. The most widely used type of equilibrium is the Nash equilibrium, named after John Nash, who introduced it in his 1950 paper “Equilibrium Points in N-Person Games.” It was popularized by the 1994 film “A Beautiful Mind,” which depicted Nash’s life and work.

It is defined as a set of strategies where no player can improve their payoff by unilaterally changing their strategy, assuming others keep their strategies constant. In other words, a Nash equilibrium is a set of strategies where no player has an incentive to deviate from their current strategy, given the strategies of the other players.

Here are a few examples of Nash equilibria: